Google 5-Star Rated Direct Hard Money Lender

Can You Refinance a Hard Money Loan?

Your exit strategy is an essential part of your hard money loan. When your loan reaches maturity, how will you pay it off?

For many, the best choice for exiting a hard money loan is a refinancing. Refinancing allows you to turn your hard money loan into a long-term loan. You can use the proceeds of your refinancing loan to pay off your hard money loan. In some cases, you may even have funds leftover to pay off other debts or pursue future investments.

Read on to learn all about refinancing hard money loans, how it works, and what to know.

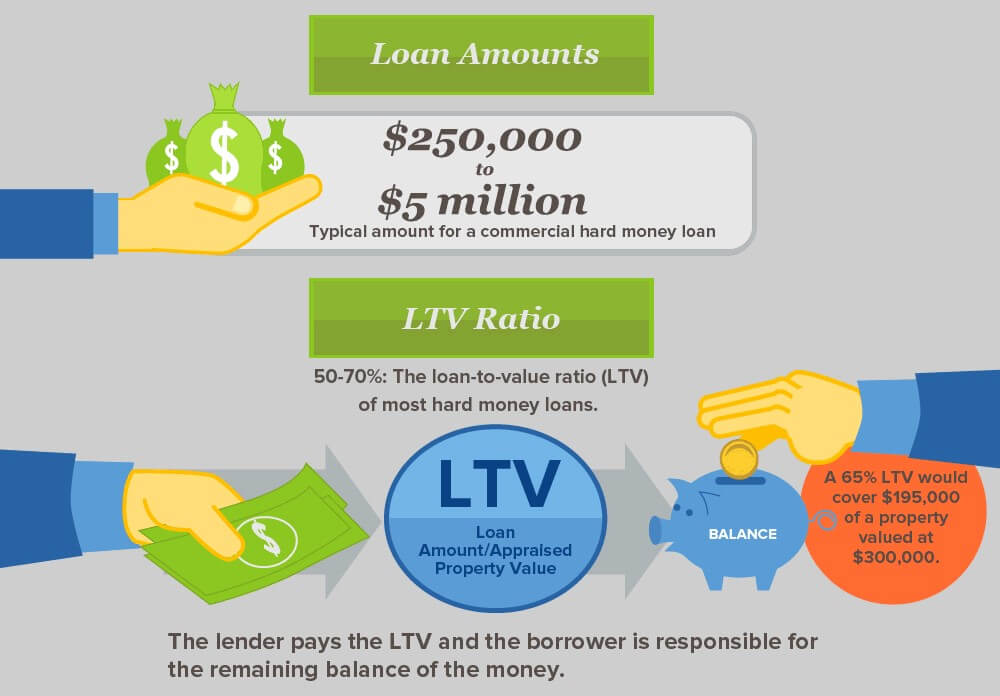

What Is a Hard Money Loan?

Hard money loans are short-term, asset-based financing secured by real estate, rather than your credit history. These loan types are typically used for real estate investing, like fix-and-flip projects, to bridge a financial gap between purchasing a new property and selling an existing one, or other property purchases.

Compared to traditional loans, hard money loans have:

- Easy qualification: Low or no minimum credit scores, as well as little or no financial documentation requirements

- Short durations: Terms are typically 12-24 months

- Fast closing: Loans can close in as little as 10 days

- Higher interest rates: Usually between 8% and 15% to compensate for higher risk

While conventional mortgages rely on a borrower’s creditworthiness and extensive financial documentation, hard money lenders are solely focused on the value of your collateral property.

Why Consider Refinancing a Hard Money Loan?

Hard money loans are excellent solutions for short-term financing, but they’re not a permanent solution. In addition to the very brief terms, these loans can have higher interest rates that simply don’t make sense long term. By refinancing a hard money loan, you can find a financially feasible solution for the long term.

Refinancing a hard money loan offers a range of benefits, including:

- An extended payment timeline: By refinancing a hard money loan, you can extend its payment timeline from 12 to 24 months to 15+ years.

- Eased monthly cash-flow pressures: Due to their high interest rates and short terms, monthly payments for hard money loans can be very high. Refinancing into a traditional loan can result in a more manageable monthly payment.

- Avoid balloon payments: If your hard money loan doesn’t have monthly payments, you’ll likely be facing a balloon payment of the entire loan amount at the end of your lending term. By refinancing your loan, you can avoid paying this out of pocket.

- Consolidate high-cost debt: If you have several different hard money loans or other high-cost debt, refinancing can help you consolidate all your debt into a single monthly payment with more favorable terms.

When Is a Hard Money Refinance Feasible?

The more value your property holds, the more successful your refinance will be, so it’s best to wait until your property has increased in value due to market gains or completed improvement. Typically, you’ll need at least 20% equity in your property in order to refinance your hard money loan. If you can increase your equity to between 25% and 35%, even better.

You’ll also need to be in good financial standing to qualify for your refinance, just like you would need to be to qualify for a mortgage outright. That means having a good credit score, a low debt-to-income ratio, and consistent proof of income.

Benefits of Refinancing a Hard Money Loan

Why might you want to refinance your hard money loan? Read on to learn what a refinance can do for you.

Lower Interest Rates and Loan Origination Fees

Traditional loans are considered much lower risk than hard money loans and have interest rates to reflect that. Refinancing may result in a 2-5% reduction in your interest rate. Though it may sound menial, this rate reduction can translate into thousands saved in interest over just a few years.

Extended Repayment Terms and Reduced Monthly Payments

Thanks to the much longer terms of your refinanced loan, you can expect a significant drop in monthly payments. A refinance can free up cash to be used for maintenance, new acquisitions, or to pay off other debts.

Consolidating Debt and Improving Cash Flow

When you refinance your hard money loan, you can refinance other high-rate loans along with it, like tax liens or credit lines. In doing so, you can streamline your debt into a single monthly payment, rather than juggling multiple repayment schedules. You can also get more favorable interest rates.

Step-by-Step Hard Money Refinance Process

Wondering how it works? Here’s what to expect when refinancing your hard money loan into a traditional mortgage:

-

- Research your lenders: Take the time to compare multiple lenders to find the most favorable terms. Ask for references from friends and family, read online reviews, or research the Better Business Bureaus’ website.

- Gather documentation: You’ll need to compile your current loan information, proof of insurance, tax returns, bank statements, and other financial information.

- Submit your application: Complete your lender’s application and submit any necessary documentation.

- Underwriting and appraisal: During this process, your lender will review your application and qualify you for a loan. They’ll also order an appraisal of your property.

- Loan approval: If you meet your lender’s requirements, they’ll conditionally approve your loan.

- Disclosure review: You’ll have a chance to review your loan terms and all costs associated with your loan.

- Close: You’ll sign loan paperwork and receive funding. A portion of this funding will be used to pay your existing loan.

Common Mistakes When Refinancing Hard Money Loans

Refinancing your hard money loan? Don’t make these common mistakes.

Underestimating Closing Costs and Origination Fees

Interest rates are a big part of the puzzle when it comes to understanding the cost of a loan, but they’re not all that matters. Focusing solely on interest rates can leave you with a big bill you didn’t expect. Be sure to look at other figures like closing costs and loan origination fees when determining the value of your refinance.

Not Considering Your Options

Your refinancing loan is a several-decade commitment, so it’s vital that you find one that meets your needs. In addition to comparing lenders’ terms, consider whether they’re a lender you’d like to work with for the long term. Then, do your due diligence to ensure a strong reputation.

Ignoring the Market

Market conditions have a huge impact on the terms of your refinancing loan, so it’s important to pay attention to them. Strike when terms are favorable for your best possible outcome, but don’t wait so long for a market swing that you miss your hard money loan maturity date.

Frequently Asked Questions

Can I Refinance with Bad Credit?

While your credit score may not have mattered when you applied for your hard money loan, it plays a significant role in your refinance. Most traditional lenders require a minimum credit score around 600 to qualify.

How Long Does Hard Money Refinance Take?

The traditional lending process takes much more time than a hard money loan. To make sure you secure your refinancing loan within the terms of your hard money loan, plan at least 3 months for the refinance.

What Fees Are Associated with Hard Money Refinance?

Refinancing loans include a number of different fees, including lender fees like application fees, underwriting fees, and document preparation fees, as well as third-party appraisal, recording, and attorney fees and more.

Can I Switch Lenders During Refinance?

If you find that your refinancing lender isn’t meeting your needs, you can switch lenders during the process. You’ll need to inform your current lender of your intent to change and undergo the application process with your new lender.

Conclusion: Refinancing Hard Money Loans Demystified

Refinancing your hard money loan can transform your high-cost, short-term loan into a long-term loan with favorable rates, freeing up cash flow and allowing for long-term financial feasibility. That said, it’s important to choose your refinancing lender carefully. Weigh all costs, compare lenders, and allow yourself plenty of equity to protect against market shifts.

")